April 2013 Dealer Profitability

Amelia Taylor | 30 May 2013

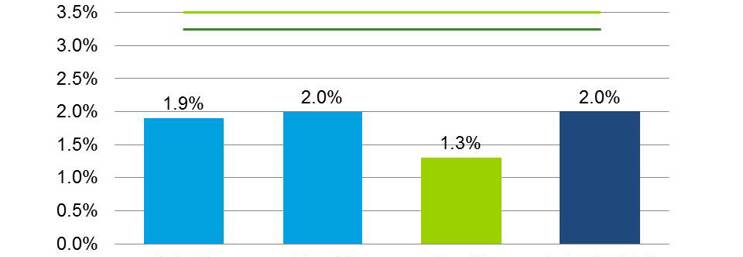

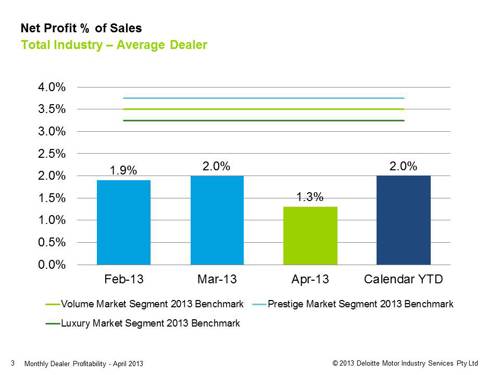

Total industry

- The total industry experienced a decline in average dealer profitability this month following a slower than usual March. At 1.3% the industry is well below all of the individual market segment benchmarks by at least 2 percentage points.

State by State

- The average dealer in every region declined barring the SA&NT area that remained the same this month. This is a feat considering the challenging conditions that dealers are currently experiencing

- The largest decline in profitability was experienced by NSW&ACT and WA. These states experienced a decrease in profit by 0.7 percentage points. At 0.8% this is the lowest profitability the average NSW&ACT dealer has experienced since July 2011. For the average WA dealer last April was the most recent time that their profitability dropped to 1.8%.

Segments

- All three segments experienced a decline in NP%S this month, with the greatest decrease happening in the luxury market

- This is the lowest that profitability has fallen to in all segments, on a monthly basis, for the past year and a half.

Click the graph below to see full profitability presentation

General Information Only

This presentation contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively the “Deloitte Network”) is, by means of this presentation , rendering professional advice or services.

Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this presentation.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which are separate and independent legal entities, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Hanoi, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Osaka, Seoul, Shanghai, Singapore, Sydney, Taipei and Tokyo.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.