September 2014 Dealer Profitability

Deloitte Motor Industry Services | 1 October 2014

Total Industry

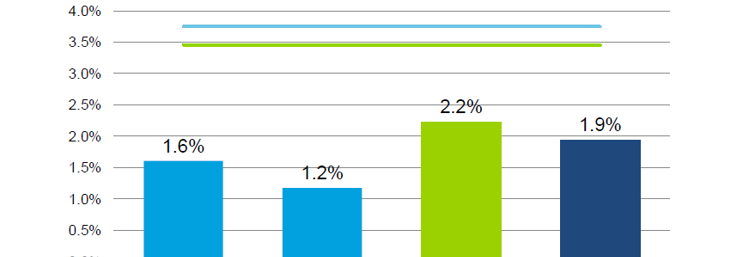

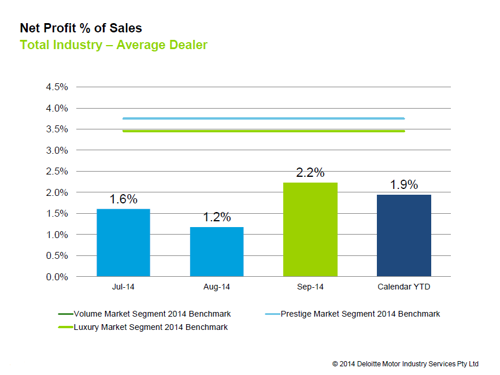

Dealer profitability as measured by net profit as a percentage of sales (NP%S) was 2.2% for the average Australian dealer in September 2014.

The uplift on last month can be partly attributed to quarterly new car incentive payments earned per unit which were up 36% month-on-month. However, the September 2014 result was still 0.4 percentage points above the September 2013 result last year which also benefited from quarterly new car incentives at the time.

The September month’s result was also 0.3 percentage points above the calendar YTD NP%S level of 1.9%.

State-by-State

New South Wales/Australian Capital Territory

In September, the average NSW/ACT dealer saw a NP%S of 2.2%, up from the 1.3% result in August, and also 0.7 percentage points better than September 2013. This uplift in September can be attributed to stronger new vehicle department performance including the impact of quarterly new car incentive payments which were 31% above the calendar YTD figure. In turn, new vehicle gross margin was 7.3% in September for the average NSW/ACT dealer, which was 0.3 percentage points above the calendar YTD figure. This impacted the department’s overall profitability with selling gross (gross profit less selling expenses not including overheads) as a percentage of gross for the average dealer at 15% – the highest result in the year so far excluding June 2014.

Queensland

With an NP%S of 2.6%, QLD was the most profitable state for the September month. New vehicle department gross margins were strong for the average dealer in the state at 7.9%, with this in part being reflective of quarterly new car incentive payments which were up 31% in September on the calendar YTD figure. Furthermore, QLD also performed strongly in finance & insurance (F&I) with $1,275 of F&I income earned per vehicle retailed which was $161 above the industry average. This was a reflection of QLD being the only state to have both finance penetration and income per contract figures above the industry average.

South Australia/Northern Territory

The average SA/NT dealer returned 2.4% NP%S in September. The state had the strongest total dealership gross margin at 14.7% which was 1.5 percentage points above the industry average. This above average performance can be attributed to the state grouping continuing to have strong pure grosses (new car gross profit excluding incentives, holdback and aftermarket) that were then enhanced with incentives this month. Conversely, the service department performance for the average SA/NT dealer was below the rest of the industry in September with selling gross as a percentage of gross at 54% compared to the national average of 56%. This figure is a reflection of softer gross margins in the state with the average SA/NT dealer returning 61% gross profit as a percentage of sales compared to the industry average of 64%.

Victoria/Tasmania

Dealer profitability for the average VIC/TAS dealer improved month-on-month with NP%S for September at 1.6%, representing a 0.9 percentage point increase on the August result. With total expenses (as a % gross) continuing to be below the industry average, improvements in gross income (traditional department gross profit and F&I income) this month contributed to the improvement in dealer profitability overall. Notably, VIC/TAS dealers have been steadily moving their F&I performance closer to the industry average over the past year. In September, the average VIC/TAS dealer earned $761 in finance income per retail vehicle sold– $155 more per vehicle than in January 2014. This compares to the industry average which only increased by $50 over the same period.

Western Australia

NP%S for the average WA dealer was 1.0% in September making it the only state to fall in profitability when compared to the previous month. As market volumes for the state are down on prior year, new vehicle grosses including aftermarket, holdback and incentives have also been declining across the 2014 calendar year. Gross per new vehicle sold including aftermarket, holdback and incentives was $2,098 for the average WA dealer in September 2014 - $462 less than the January 2014 result. The reduction in gross made it harder for the average WA dealer to cover fixed costs, ultimately impacting the bottom line.

Segments

- NP%S for the average dealer in the volume segment was 1.8%in September. It was the only segment to have its NP%S result for the month fall below its calendar YTD result of 1.9%.

- The prestige segment returned an average NP%S of 2.0% in September. The prestige segment’s calendar YTD result remains the highest of the segments, with a difference of 0.03 percentage points between it and the luxury segment.

- The luxury segment was the most profitable state in September with an NP%S of 2.3%. This was an increase of 0.6 percentage points on the dealer profitability result for September 2013.

Please click the image below for more details.

General Information Only

This presentation contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively the “Deloitte Network”) is, by means of this presentation , rendering professional advice or services.

Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this presentation.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which are separate and independent legal entities, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Hanoi, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Osaka, Seoul, Shanghai, Singapore, Sydney, Taipei and Tokyo.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.