Leading Indicators of Profitability

Balram Dabhade | 17 May 2017

Why Use Leading Indicators?

Leading indicators are designed to flag potential problems early, so that preventive action can be taken. It also helps to identify your areas of improvement, where you can focus resources in time to prevent undesirable business outcomes.

In this series, we will publish during the course of the next month key KPIs that provide a predictive sense of profitability, equipping your dealership to be agile and change course timeously.

This study was conducted across data from over 1000 dealerships across three years (2013- 2015) within Australia using the Deloitte proprietary database eProfitFocus.

New Vehicle Inventory

The first leading indicator we intend to explore is New Vehicle Stock Holding and its effect on profitability.

We studied over 1000 vehicle dealerships from our eProfitFocus database, selling different brands, from different segments across Australia over three years and observed that irrespective of your location, size and turnover, how you manage your new vehicle inventory, has a direct effect on your profitability.

New vehicle stock is tricky to manage, as it involves multi-faceted pulls and pushes from different stakeholders (Customers, Franchises, Finance companies etc). Some would argue that you should hold just-in-time inventory, which may be desirable in a perfect world.

However we observed that new vehicle inventory ageing is a controllable KPI, and if managed correctly, can often lead to better results.

We segmented the industry into

- Top30% dealers by NP%S,

- Average dealers and

- Loss making dealers

to study their new inventory holding pattern and also studied the inventory holding pattern to predict if the dealership would be a profitable dealership or otherwise.

This study found a dependency of dealership profitability on new vehicle stock management.

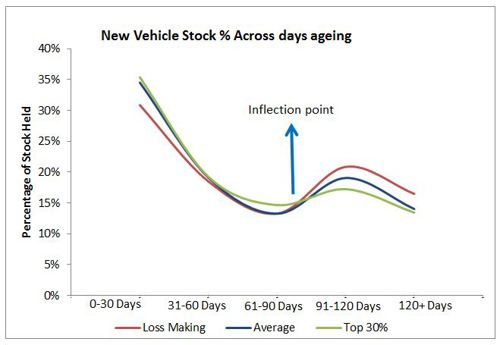

We observed that the profitable dealers engaged in an “Accelerated stock depletion” model, where they held 5% - 6% more inventory than the loss making dealers in the 0-60 days’ time period. They also sold this inventory at a faster rate than the loss making dealers in this time frame.

We noted that 90 days was the point of inflection; this was the time frame after which the differentiation of profitable dealer’s versus the loss making dealers was clearly visible.

The profitable dealers do not let more than 30% of their total stock pass the 90 days ageing barrier, as opposed to the loss making dealers, who were seen to often hold aged stock greater than 90 Days.

Actions that the Profitable dealers take:

- Manage optimum stock throughput

- Demand planning for 1 month, 3 months and 6 months

- Accelerated stock depletion

- Effective use of people and monetary resources to prevent stock ageing

As this leading Indicator series continues, we plan to dive deeper into the data, to understand the factors that affect the profitability of vehicle dealerships across Australia further.

Stay tuned for more on the other Leading Indicators in our next publications.

If you wish to know more about our benchmarking and analytical processes and how you can gain from these, we would be pleased to discuss this with you.

Contacts:

General Information Only

This presentation contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively the “Deloitte Network”) is, by means of this presentation , rendering professional advice or services.

Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this presentation.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte Asia Pacific Limited is a company limited by guarantee and a member firm of DTTL. Members of Deloitte Asia Pacific Limited and their related entities, each of which are separate and independent legal entities, provide services from more than 100 cities across the region, including Auckland, Bangkok, Beijing, Hanoi, Hong Kong, Jakarta, Kuala Lumpur, Manila, Melbourne, Osaka, Seoul, Shanghai, Singapore, Sydney, Taipei and Tokyo.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms or their related entities (collectively, the “Deloitte organization”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser.

No representations, warranties or undertakings (express or implied) are given as to the accuracy or completeness of the information in this communication, and none of DTTL, its member firms, related entities, employees or agents shall be liable or responsible for any loss or damage whatsoever arising directly or indirectly in connection with any person relying on this communication. DTTL and each of its member firms, and their related entities, are legally separate and independent entities.